Bridging Loan Guide – A bridging loan is short-term property finance used when timing matters. It can help buyers, homeowners, landlords, investors and businesses bridge a gap between needing funds now and arranging a longer-term repayment route later.

This guide explains how bridging loans work, when they may be useful, what they can cost, what lenders usually assess and why a clear exit strategy matters. It also explains how Connect supports a wider property finance journey through residential mortgages, buy-to-let, commercial finance, second charges, development finance and adviser support.

Bridging finance is not suitable for every situation. It is usually more expensive than a standard mortgage and is normally secured against property. You should understand the risks, costs and repayment route before proceeding.

What is a Bridging Loan?

A bridging loan is a short-term loan secured against property or land. It is designed to provide temporary funding when a borrower needs to complete quickly, unlock equity, buy before selling, refurbish a property or arrange finance before moving to a longer-term mortgage.

The lender takes a legal charge over the property used as security. If the loan is not repaid as agreed, the secured property may be at risk.

Bridging loans are often used where a standard mortgage is too slow, unavailable at the start, or unsuitable until a property or transaction reaches a later stage. For example, a property may need refurbishment before it qualifies for a long-term mortgage, or a buyer may need to complete an auction purchase within a fixed deadline.

For borrowers who need a longer-term mortgage rather than short-term finance, our residential mortgage guide explains how standard home loans work.

When Can a Bridging Loan Be Useful?

A bridging loan may be considered when there is a clear short-term need and a realistic repayment plan. Common uses include:

- Buying a property before selling an existing property

- Completing an auction purchase within a tight deadline

- Funding a property chain break

- Purchasing a property that needs refurbishment before mortgage completion

- Raising funds against an existing property for a short period

- Supporting buy-to-let, commercial or semi-commercial property transactions

- Refinancing short-term borrowing into a longer-term mortgage later

A bridging loan should not be treated as a simple replacement for a standard mortgage. It is usually used when speed, timing, property condition or transaction structure makes short-term finance more appropriate.

If the project involves major building work, staged drawdowns or a full development scheme, development finance may be more suitable than a bridging loan.

How does a bridging loan work?

A bridging loan works by giving the borrower access to short-term funds secured against property. The lender reviews the property, the purpose of the loan, the borrower’s position, and the proposed exit strategy.

The process usually follows these stages:

- The borrower explains why short-term finance is needed.

- The adviser or lender reviews the property, security and timescale.

- A valuation confirms the property value and suitability.

- Legal checks confirm ownership, charges and security position.

- The lender issues terms if the case fits its criteria.

- Funds are released once legal work and conditions are complete.

- The loan is repaid through the agreed exit route.

The exit route is central to the application. This could be the sale of a property, a residential mortgage refinance, a buy-to-let mortgage, a commercial mortgage, or another acceptable repayment source.

Types of Bridging Loans

Closed bridging loan

A closed bridging loan has a known repayment date or a clearly defined repayment event. This may be a confirmed property sale or an agreed refinance. Lenders often view closed bridging loans as lower risk because the repayment plan is clearer.

Open bridging loan

An open bridging loan does not have a fixed repayment date. The borrower still needs a credible exit strategy, but the timing may be less certain. Open bridging loans can carry higher risk and may cost more.

First charge bridging loan

A first charge bridging loan is secured against a property with no existing mortgage, or where the bridging lender will hold the first legal charge. This gives the lender first claim over the property if the loan is not repaid.

Second charge bridging loan

A second-charge bridging loan is secured against an existing mortgage. The existing mortgage lender keeps the first charge, and the bridging lender takes a second charge. This can be useful where the borrower wants to keep their current mortgage in place, but it may be more complex and more expensive.

For some homeowners, a second charge mortgage may be a longer-term alternative. You can learn more through our adviser services and support pages.

What Can a Bridging Loan Cost?

Bridging loan costs vary by lender, property type, loan-to-value, risk, loan purpose and exit strategy. The main costs may include:

- Monthly interest

- Arrangement fee

- Valuation fee

- Legal fees

- Broker fee, where applicable

- Exit fee, where charged

- Administration or title-related costs

Bridging finance is usually priced monthly because it is short-term finance. Interest may be paid monthly, retained from the loan at the start, or rolled up and repaid at the end. The structure depends on the lender and the borrower’s circumstances.

A lower loan-to-value ratio, strong security, and a clear exit route may improve the options available. A higher-risk case, an uncertain exit strategy, or a complex property may increase costs.

Borrowers should not compare bridging loans only by headline rate. The total cost of borrowing matters, including fees, retained interest, legal work, valuation and any exit charges.

What is an exit strategy?

An exit strategy is the planned method for repaying the bridging loan. It is one of the most important parts of a bridging application.

Common exit strategies include:

- Selling the property used as security

- Selling another property

- Refinancing to a residential mortgage

- Refinancing to a buy-to-let mortgage

- Refinancing to a commercial mortgage

- Repaying from agreed business or investment funds

- Moving to development finance or longer-term property finance, where suitable

A weak exit strategy can make it difficult to secure a bridging loan. It can also increase the risk of delays, extra interest and financial pressure.

If your planned exit is a remortgage, our remortgage guide explains how refinancing works and what lenders may assess.

Eligibility criteria for bridging loans

Lenders usually assess the full case rather than only income or credit score. They may review:

- Property value and condition

- Loan amount and loan-to-value

- Exit strategy

- Borrower experience

- Credit history

- Income position, where relevant

- Legal title and existing charges

- Property location

- Purpose of funds

- Timescale for completion and repayment

Some bridging loans are regulated by the Financial Conduct Authority when they are secured against a property that the borrower or a close family member lives in or intends to live in. Investment and commercial bridging loans are often unregulated. This distinction is important, and borrowers should take suitable advice before proceeding.

Bridging Loan Examples

Buying before selling

A homeowner may want to buy a new home before their current property sale completes. A bridging loan may help complete the new purchase, with repayment planned from the sale of the existing home.

Auction purchase

Auction buyers often have strict completion deadlines. A bridging loan may help complete the purchase quickly, especially where a standard mortgage cannot complete in time.

Refurbishment before refinance

A landlord may buy a property that needs work before it can be let or refinanced. Bridging finance may fund the purchase or works before the borrower refinances to a longer-term buy-to-let mortgage.

Commercial property timing gap

A business owner or investor may need short-term finance to secure a commercial property, complete a refurbishment or bridge the gap before arranging longer-term commercial finance.

Property that is not mortgage-ready

Some properties may not qualify for a standard mortgage immediately due to condition, missing facilities or required works. Bridging finance may be considered where there is a clear plan to improve the property and refinance later.

Benefits of bridging loans

A bridging loan may offer:

- Faster access to finance than some standard mortgage routes

- Flexible short-term borrowing

- Support for auction and time-sensitive purchases

- Funding for refurbishment or property improvement

- A route to buy before selling

- Options for residential, buy-to-let and commercial property cases

- A temporary solution before sale or refinance

The benefit depends on the borrower having a clear purpose, suitable security and a realistic repayment plan.

Risks of Bridging Loans

Bridging loans carry risks. These include:

- Higher costs than many standard mortgages

- Interest building quickly if repayment is delayed

- Legal and valuation costs even if the case does not complete

- Risk of repossession if the loan is not repaid

- Pressure if the property sale or refinance takes longer than expected

- Possible exit fees or early repayment charges, depending on the lender

A bridging loan should only be used when the borrower understands the costs, timescale and repayment route.

Bridging Loan or Development finance?

Bridging loans and development finance are both short-term property finance options, but they are not the same.

A bridging loan is often used for a purchase, chain break, auction deadline, light refurbishment or short-term refinance. It is usually advanced as one facility and repaid through sale or refinance.

Development finance is usually used for heavier property projects, structural works, conversions, new builds or schemes where funds are released in stages. Lenders may assess planning permission, gross development value, build costs, contractor experience and monitoring reports.

If the works are light and the exit route is clear, bridging finance may be enough. If the project involves structural work, staged construction or a full development plan, development finance may be more appropriate.

How an Adviser Can Help with Bridging Finance

A bridging loan adviser can help assess whether short-term finance fits the case. They can explain how different lenders may view the property, loan purpose, exit route and timescale.

An adviser may help with:

- Comparing lender criteria

- Understanding regulated and unregulated bridging

- Reviewing the exit strategy

- Explaining likely costs and fees

- Checking whether a mortgage, remortgage, second charge or development finance option may be better

- Preparing the case for lender review

- Managing communication between lender, solicitor and valuer

Borrowers can use Connect Experts to find a residential bridging loan adviser by adviser preference, language and location.

For business property or commercial short-term borrowing, Connect Experts also offers a commercial bridging loan adviser search.

Why Connect Supports More Than Bridging Finance

Bridging loans are one part of a wider property finance journey. A borrower may start with short-term finance, then move to a residential mortgage, buy-to-let mortgage, commercial mortgage, second charge mortgage or development finance facility.

Connect is built to support that wider journey. Through the Connect network, advisers can access support across mainstream and specialist lending, including residential mortgages, buy-to-let, commercial finance, bridging finance, second charges, development finance, protection and general insurance.

This matters because many property cases do not fit neatly into one product category. A client may begin with a bridging need but later require a remortgage, landlord finance, commercial lending or protection advice. A complete network gives advisers and clients a broader route through the full property finance lifecycle.

Experienced brokers who regularly handle complex or time-sensitive property cases can also explore joining Connect Network to access lender, compliance, technology, placement, and case management support.

Alternatives to a bridging loan

A bridging loan may not always be the right option. Alternatives may include:

- A residential mortgage

- A remortgage

- A further advance

- A second charge mortgage

- A buy-to-let mortgage

- A commercial mortgage

- Development finance

- Business finance

- Delaying the purchase until the sale completes

The right route depends on the property, purpose, timescale, affordability, security and repayment strategy.

Questions to ask before choosing a bridging loan

Before applying, consider:

- Why do I need short-term finance?

- What property will secure the loan?

- How much do I need to borrow?

- What is the loan-to-value?

- How long do I need the finance for?

- What is my exit strategy?

- What happens if the sale or refinance is delayed?

- What are the total costs, not just the interest rate?

- Is the loan regulated or unregulated?

- Are there more suitable alternatives?

Clear answers can reduce delays and help an adviser or lender assess whether bridging finance is suitable.

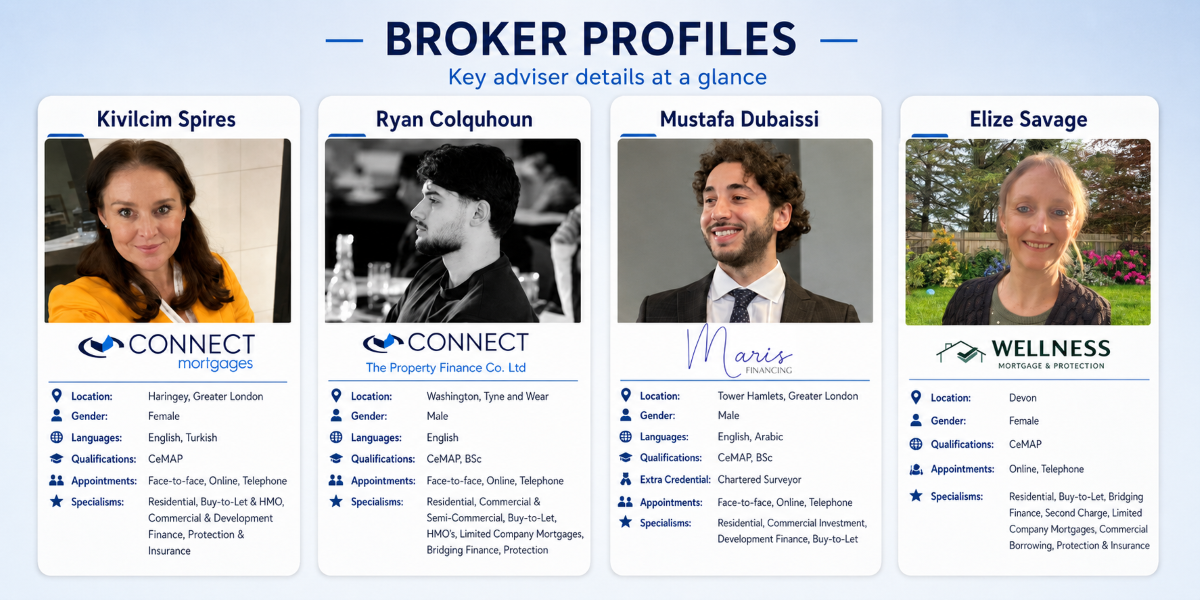

To see the full extent of our Bridging Loan Brokers, click the broker profiles below!

Bridging loan FAQs

| Question | Answer |

|---|---|

| How quickly can a bridging loan complete? | Some bridging loans can complete quickly, but timing depends on valuation, legal checks, lender requirements and the complexity of the property. Auction and urgent cases may move faster when documents are ready and the exit route is clear. |

| How long does a bridging loan last? | Many bridging loans run from a few months up to 12 or 24 months, depending on the lender and case. The term should match the borrower’s realistic repayment plan. |

| Can I get a bridging loan with poor credit? | It may be possible, depending on the lender, property security, loan-to-value and exit strategy. Poor credit can reduce lender choice and increase costs. |

| How much can I borrow with a bridging loan? | The amount depends on the property value, available equity, lender criteria, loan purpose and exit route. Lenders usually assess the loan-to-value and the strength of the security. |

| Do I need an exit strategy? | Yes. A bridging loan normally requires a clear exit strategy. This may be sale, refinance or another acceptable repayment route. |

| Can I use a bridging loan for auction property? | Yes, bridging finance is often used for auction purchases because completion deadlines can be short. The borrower still needs suitable security and a repayment plan. |

| Can a bridging loan fund refurbishment? | Yes, bridging finance may support light refurbishment or property improvement. Heavy structural work may require development finance instead. |

| Is bridging finance regulated? | Some bridging loans are regulated, usually when secured against a property the borrower or close family member lives in or intends to live in. Investment and commercial bridging loans are often unregulated. |

| Can I refinance a bridging loan into a mortgage? | Yes, this is a common exit strategy. The borrower may refinance into a residential, buy-to-let or commercial mortgage if the property and borrower meet lender criteria. |

| What happens if I cannot repay the bridging loan? | If the loan is not repaid, interest and charges may increase. The lender may also take enforcement action, and the secured property may be at risk. |

| Is a bridging loan better than a mortgage? | Not usually for long-term borrowing. A standard mortgage is often cheaper for long-term finance. A bridging loan is normally used when short-term timing, property condition or transaction structure creates a specific need. |

| Should I use a bridging loan adviser? | Advice can be valuable because bridging finance varies widely by lender, property type, security, exit route and regulation. An adviser can help compare options and explain risks before you proceed. |