Second charge mortgage fees cannot be assessed by comparing headline costs alone.

The advice process may involve affordability checks, property equity, existing lender consent, valuations, credit evidence, debt statements and alternative borrowing options.

Advisers must explain every charge, assess fair value and show why the recommendation meets the client’s needs.

Why Second Charge Mortgage Fees Require Context

A fee only becomes meaningful when the work behind it is understood.

Second charge mortgages sit behind an existing mortgage. The first charge remains in place, while a separate lender takes an additional legal charge over the property.

This structure can make the advice and application process different from a standard remortgage.

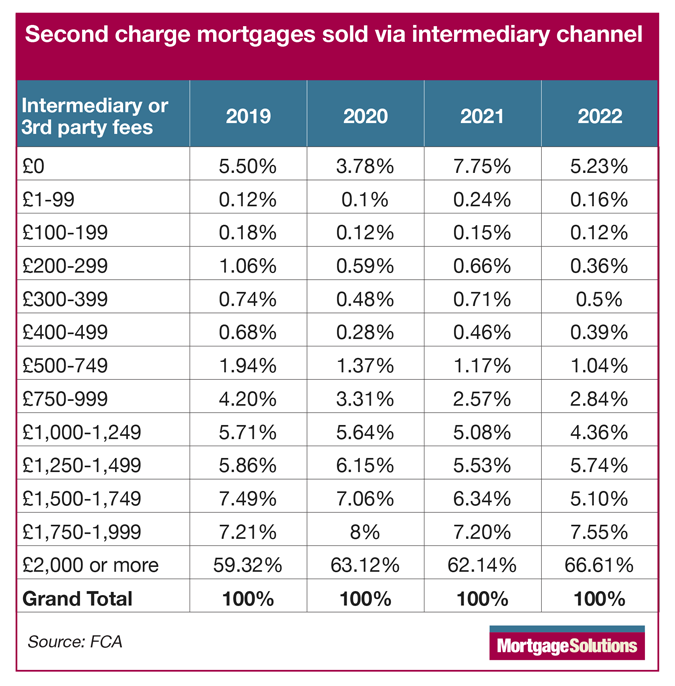

Historic FCA data obtained through a Freedom of Information request showed that 67% of brokered second charge loans in 2022 involved fees of £2,000 or more. The equivalent figure was 59% in 2019.

These figures provide a useful historic market reference. However, they do not establish what every adviser or borrower will pay. Individual charges depend on the service, loan requirements and case complexity.

What Work Can Sit Behind the Fee?

A second charge recommendation may require an adviser or specialist firm to complete several checks before submission.

These can include:

- Reviewing the existing mortgage balance and product terms

- Checking for early repayment charges

- Establishing the available property equity

- Assessing income, expenditure and credit commitments

- Calculating combined loan-to-value

- Reviewing the purpose of the borrowing

- Obtaining statements for debts being repaid

- Checking whether the first charge lender’s consent is required

- Arranging an automated, desktop or physical valuation

- Reviewing title restrictions or property-related concerns

- Comparing the second charge with other suitable borrowing routes

The adviser must also consider whether the proposed repayment remains affordable alongside the existing mortgage.

Connect Network members can use the Second Charge Help Desk when a case requires specialist placement or further technical support.

Regulatory Changes in the Second Charge Market

The second charge mortgage industry has seen significant regulatory transformation over the past decade. Since 2016, second charges have been brought under the FCA’s mortgage regulatory framework, tightening expectations on compliance, advice standards, and transparency.

In 2018, the FCA issued a formal communication to lender CEOs, citing “significant issues” in second charge lending practices. Firms were strongly encouraged to review and enhance their operational procedures, ushering in a new era of compliance, customer duty, and adviser accountability.

As we move further into 2025, these trends remain relevant. With rising costs and heightened scrutiny, advisers must ensure they operate under a robust compliance framework, especially when placing second-charge deals.

📘 Need tailored support in today’s regulated landscape? Visit our Mortgage Adviser Support Hub to access compliance tools, AI-powered case support, and exclusive training resources.

First and second charge mortgages’ fee structuresare incomparable

She said it’s important not to compare fees for first- and second-charge mortgages, as the “skills, process, knowledge and amount of work required are completely different.”

Nicholas Mendes, mortgage technical manager at John Charcol, agreed that approval processes were more manual for second charge, adding that less technology was used to automate parts of the approval process.

He added that rising fees could also be attributed to higher demand and tighter lending criteria, driven by rising rates and squeezed affordability.

Operational expenses on the rise for second charge mortgages

According to Positive Lending’s CEO, Paul McGonigle, the prevailing narrative suggests that two-thirds of borrowers are paying £2,000 or more. However, he clarified that his firm’s experience paints a different picture, with the average fee falling from £1,000-1,249.

McGonigle emphasised that larger fee-charging firms like his cover the client’s mortgage survey and reference request costs and absorb losses from down-valuations without passing the burden to the client.

Taking a pragmatic stance, he expressed that if mortgage brokers adopted a similar approach, it could significantly increase average mortgage fees.

Acknowledging the increased complexity and expenses associated with second charge mortgages, McGonigle highlighted an 11% rise in operational costs for this product line. Despite this, he affirmed that Positive Lending has shouldered most of these costs while remaining profitable.

The FCA will inquire about the primary beneficiary of the deal

The FCA is set to examine who stands to gain the most from a deal, questioning whether it’s the broker or the customer. According to Robert Sinclair, CEO of the Association of Mortgage

For intermediaries, the customer might not benefit significantly from the arrangement, especially if they’re borrowing existing funds and incurring broker fees. This practice could obscure higher fees, potentially reaching £3,000 or more.

Sinclair emphasises the need to address transparency issues in the sector. He points out that justifying the value and fees requires scrutiny of the work involved.

He questions the allocation of tasks between experienced advisers and administrative staff, noting that clerical personnel handle much of the work in second-charge mortgages, including legal documentation and settling existing debts.

In addition, Sinclair raises concerns about the concentration of business within a few key players in the sector. He suggests that this concentration allows the regulator to understand the landscape, prompting further examination into the practices and justifications for fees within these select entities.

Why First and Second Charge Fees Differ

A first charge mortgage and a second charge mortgage should not be compared solely by their broker fees.

With a standard remortgage, the new loan usually replaces the existing mortgage. A second charge keeps the original mortgage and adds another secured commitment.

This creates a different assessment.

The adviser may need to examine:

- The cost of retaining the current mortgage

- The total cost of the second charge

- Two separate monthly mortgage payments

- The repayment period for each loan

- Any early repayment charges

- The effect of extending debt over a longer term

- The client’s future plans for the property

The right question is not simply which product has the lowest initial fee. It is which suitable option produces an acceptable overall outcome.

Alternatives Advisers Should Consider

A second charge should not be treated as the automatic answer whenever a client wants to release equity.

Depending on the circumstances, alternatives may include:

- A further advance from the existing lender

- A full remortgage

- An unsecured personal loan

- Retaining existing debts

- Delaying the proposed expenditure

- Using available savings

- A different form of specialist finance

Each route can produce a different interest cost, monthly payment, term and level of security.

For example, retaining a competitive first-charge rate could support a second-charge recommendation. However, a remortgage may be more suitable where the overall cost is lower after fees and early repayment charges.

Fee Disclosure and Fair Value

Advisers should explain fees before the client becomes committed to the transaction.

The explanation should identify:

- Who receives each fee

- When it becomes payable

- Whether it is refundable

- Whether it is added to the loan

- Whether interest will be charged on an added fee

- Which services the fee covers

- Any lender, valuation or legal charges

Adding a fee to the loan can reduce the immediate cash requirement. However, it may increase the amount repaid because interest can apply throughout the term.

A clear suitability record should connect the work completed, the charge made and the value received by the client.

Connect ARs can obtain wider guidance through the network’s mortgage compliance support, including support with advice standards, file quality and client outcomes.

Debt Consolidation Needs Additional Care

Second charge mortgages are sometimes used to consolidate unsecured borrowing.

This can reduce the combined monthly payment, particularly where debts are moved over a longer term. However, a lower monthly payment does not always mean a lower total cost.

The adviser should assess:

- The total amount repayable

- The proposed mortgage term

- Interest charged over that term

- Which debts will be repaid

- Whether accounts will be closed

- The reason the debts accumulated

- The risk of further unsecured borrowing

- The effect of converting unsecured debt into secured debt

This assessment should be clear enough for the client to understand both the immediate benefit and the longer-term consequence.

The Role of Specialist Network Support

Not every adviser regularly handles second charge cases.

A mortgage network should therefore provide a suitable route for advisers who need help with lender criteria, packaging, compliance or case placement.

Connect provides a specialist second charge referral service for brokers who prefer to introduce a case for specialist advice and case management.

This can help ARs retain the client relationship while ensuring that the case reaches a team with relevant experience.

Where a consumer wishes to choose an adviser directly, the Second Charge Mortgage Adviser Search allows users to compare Connect Experts directory profiles by location and personal preference.

A Fee Should Reflect a Defensible Process

The price of advice should never be considered separately from the work, risk and client outcome.

Second charge cases can require more manual checks than standard mortgage applications. That does not mean every high fee is justified. Nor does it mean a lower fee always provides better value.

A sound adviser process should show:

- Why additional borrowing is needed

- Which realistic alternatives were considered

- How the recommended option meets the client’s objectives

- What the client will pay immediately and over time

- Why the service and charges represent fair value

When these points are properly recorded, the fee becomes part of an explainable advice process rather than an isolated number.

Important Information

A second charge mortgage is secured against the client’s property.

The client’s home may be repossessed if they do not keep up repayments on their mortgage or any other loan secured against it.

This publication is intended for mortgage intermediaries and provides general information rather than personal financial advice.